Your credit score impacts everything from getting a loan to securing a job, and you might be unknowingly damaging it. Are these hidden traps wrecking your financial future?

1. Late Payments on Utility Bills

Nearly 30% of Americans don’t realize that missing utility payments can be reported to credit agencies. This can lower your credit score by as much as 100 points if the debt is sent to collections.

2. Co-Signing a Loan

About 38% of co-signers end up paying off the loan themselves. If the primary borrower misses a payment, your credit score could drop by 50 to 100 points.

3. Closing Old Credit Accounts

Closing an old account can reduce your credit history length, which makes up 15% of your credit score. A shortened credit history can cause your score to drop by 20 to 30 points or more.

4. Applying for Too Much Credit at Once

Hard inquiries can decrease your score by 5 to 10 points each. Applying for multiple credit accounts in a short time frame can knock your score down by 40 points or more.

5. Carrying High Balances on Credit Cards

Credit utilization, which accounts for 30% of your score, can cause a significant dip if you exceed 30% of your credit limit. Carrying high balances can lower your score by over 100 points.

6. Ignoring Medical Bills

Unpaid medical bills account for 58% of all debt collections, according to a CFPB report. If they go to collections, it can drop your credit score by 50 to 100 points.

7. Paying Less Than the Minimum

Lenders may report this as a missed payment, which can lower your credit score by 90 to 110 points. One late payment can stay on your report for up to seven years.

8. Not Checking Your Credit Report

A 2021 study found that 34% of Americans discovered errors on their credit reports. Incorrect negative items can drop your score by over 100 points if left uncorrected.

9. Renting a Car With a Debit Card

Using a debit card for car rentals can trigger a hard inquiry, which may lower your credit score by 5 to 10 points. Always use a credit card to avoid this unnecessary hit.

10. Defaulting on Student Loans

About 15% of student loan borrowers default within three years, which can lower their credit score by 150 points or more. These negative marks stay on your report for up to seven years.

11. Having Only One Type of Credit

A mix of credit accounts makes up 10% of your credit score. Limiting yourself to just credit cards can prevent your score from growing, reducing it by up to 30 points compared to having a diverse portfolio.

12. Maxing Out Credit Cards

Maxing out your credit cards can raise your utilization ratio to 100%, leading to a score drop of 45 to 100 points. Staying below 30% utilization is recommended to avoid significant damage.

13. Not Using Your Credit Cards at All

Credit card inactivity can lead to account closure, reducing your available credit. This can cause a 15 to 25 point drop in your score due to reduced credit utilization.

14. Overdue Library Fines

Unpaid library fines sent to collections can stay on your credit report for seven years. Even a $50 fine can drop your score by 50 points or more if reported.

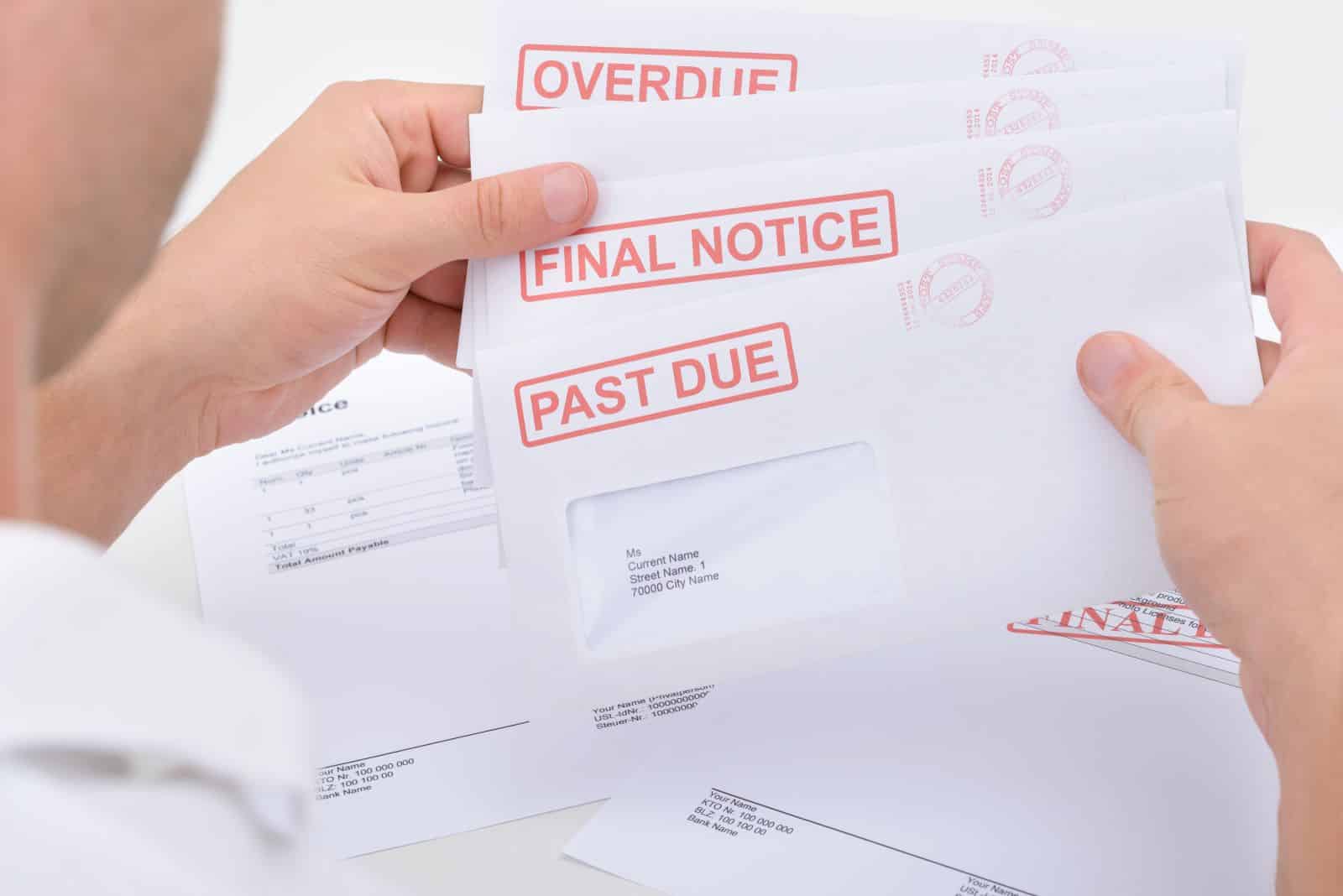

15. Ignoring Collection Notices

Debt in collections can reduce your score by 110 to 130 points. The impact is most significant in the first two years, but it lingers for seven years on your report.

16. Missing a Payment on a Small Loan

Even a single missed payment on a small loan can drop your credit score by 90 to 110 points. Payment history makes up 35% of your credit score, so staying current is crucial.

17. Overlooking a Joint Account

Missed payments on joint accounts can harm your credit just as much as your partner’s. A single missed payment on a shared account can cause a 50 to 100 point drop in your score.

18. Refinancing Loans Frequently

Every time you refinance, it triggers a hard inquiry, which can lower your score by 5 to 10 points. Frequent refinancing can lead to multiple inquiries, reducing your score by 30 points or more.

19. Failing to Pay Parking Tickets

Unpaid parking tickets sent to collections can lower your score by up to 100 points. Ignoring them won’t make them go away—they can impact your credit for up to seven years.

Protect Your Score Before It’s Too Late

Your credit score is more vulnerable than you think. Stay aware of these hidden risks, and protect your financial health before small mistakes turn into long-term problems.

Featured Image Credit: Pexels / Mikhail Nilov.

The content of this article is for informational purposes only and does not constitute or replace professional advice.

The images used are for illustrative purposes only and may not represent the actual people or places mentioned in the article.

For transparency, this content was partly developed with AI assistance and carefully curated by an experienced editor to be informative and ensure accuracy.